Header image created by Justin Lindemann

By: Justin Lindemann, Policy Analyst

In the United States, civilian nuclear power has been a part of the energy mix since 1957. Since then, nuclear energy has gone through peaks and valleys, from economic slowdowns to regulatory shifts; and recently new power plant additions have been scarce. Nevertheless, through the fresh wave of incentives, pursuits of advanced reactors, and other nuclear technologies, nuclear’s future is being given a signal of support.

Nuclear’s Past

Years after the development of the Manhattan Project to create the world’s first deployed atomic bombs, the U.S. federal government through the Atomic Energy Commission (AEC) constructed the first commercial nuclear power plant in Shippingport, Pennsylvania – which began operations in 1957 and had a 68 MW capacity until its retirement in 1982. It is important to note for those that do not know the difference between a plant and a reactor, that a reactor is the machine that controls the nuclear chain reaction for the purpose of releasing heat, while the power plant is the aggregate facility that utilizes said heat to generate electricity. As for the AEC, it no longer exists after Congress abolished the agency in 1974, as supporters and critics believed that the agency’s role should be assigned to a number of agencies, and critiques of excess regulatory requirements plagued the Commission. A year later, the era of a new regulatory agency, the Nuclear Regulatory Commission (NRC), began. The NRC, much like the AEC, has several regulatory duties that revolve around protecting public health and safety, as well as the environment. The Commission regulates and licenses civilian nuclear, as well as any associated materials. As for promotional duties, the Energy Research and Development Administration (ERDA), which became the Department of Energy (DOE), gradually took on nuclear publicity.

Although the promotion and regulation of nuclear power are primarily handled by the federal government, states also have some authority over nuclear power generation. For example, state Public Utilities Commissions are responsible for regulating the retail sale of electricity, which in part includes nuclear-based electricity, and approving cost recovery mechanisms associated with nuclear power. States also have the power to veto the location of a nuclear waste repository when it lies within their boundaries – as a result of the Nuclear Waste Act – unless the veto is overridden by Congress.

Image (above) of the Shippingport Atomic Power Station at Shippingport, Pennsylvania in 1957. (Source: Department of Energy)

Since the first civil nuclear plant in 1957, the size and capacity of commercialized nuclear has increased. Most of the country’s nuclear capacity was built between the 70s and 90s. However, the rapid build out of such energy infrastructure slowed down in the late 70s as high capital and construction costs, as well as public opposition to nuclear, dealt the expansion with several critiques. This coincided with the Three Mile Island nuclear accident in March 1979, in which one of the nuclear reactor cores partially melted due to an operating error that resulted in poor cooling circulation to the impacted core. Though there was no widespread contamination from this accident, a small fraction of radioactive material was released and the fear of further catastrophe sparked arguments against siting nuclear generation units. This influenced the NRC to place greater importance on training and active safety measures. The added attention to safety and anti-accident measures increased building and operating costs, and the stream of additional nuclear plants and reactors gradually began to stagnate, eventually reaching a slump in the 90s that has lasted into recent years.

According to the U.S. Energy Information Administration (EIA), the country reached a nuclear electricity peak of about 102,000 MW in 2012, after hovering around a 100,000 to 101,000 MW capacity for almost two decades before that. While the U.S. hasn’t seen a re-peak in almost ten years since then, electricity generation did see a massive increase even in the midst of a capacity lull. Nuclear electricity generation continued to increase from about 577,000 MWh (1990) to 769,000 MWh (2012), and peaked at 809,000 MWh in 2019. The latest operational addition to the civilian nuclear fleet was in 2016 with the grid connection of the Tennessee Valley Authority’s (TVA) Watts Bar Unit 2 in Tennessee. Before that, it was Watts Bar Unit 1 in 1996. The EIA’s most recent data from 2021 showed that generation was at about 778,000 MWh, with a total capacity of 95,000 MW worth of operating nuclear reactors. Even though operating reactors in recent history have fallen in sum, due to plant upgrades and modifications, capacity and generation has still for the most part been maintained. Nonetheless, globally the levelized cost of energy (LVOE) for nuclear – which is the cost of constructing a power plant and the ongoing lifetime costs for fuel and operations – increased to about $155/MWh in 2019, compared to $123/MWh a decade earlier. This is in stark contrast to the LCOE of solar PV and onshore wind, as both saw a decrease of 89% and 70% respectively from 2009 to 2019.

Nuclear’s Present

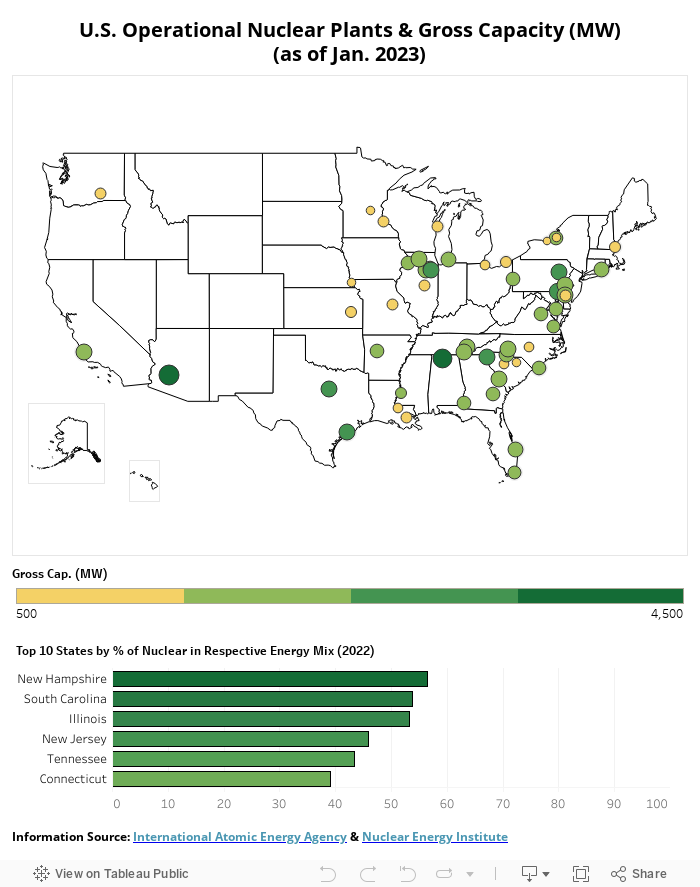

Today, per the International Atomic Energy Agency (IAEA), the U.S. has 92 individual nuclear power reactors in operation, with a total net capacity of almost 95,000 MW. The nation’s nuclear fleet makes up about 20% of the total electricity production, a number that has stayed consistent for the last 20 years and more. In terms of permanent shutdowns, the U.S. as of 2023 has seen 41 reactors be decommissioned at a total net capacity of almost 20,000 MW. The most recent shutdown was Michigan’s Palisades reactor in May 2022, which supplied the area with power since 1971.

The majority of U.S. reactors – as well as globally – are pressurized water nuclear reactors (PWR), which utilize the heat produced by nuclear energy in a reactor vessel to create steam in a secondary system that then turns a turbine connected to a generator. Others are boiling water reactors (BWR), which differ in that steam is not produced in a separate secondary system. Both of these reactor types are light water reactors, which means that they utilize normal water (which contains more of the hydrogen isotope, protium) instead of heavy water (which contains more of the hydrogen isotope, deuterium).

Diagram (above) of a Pressurized Water Reactor (PWR) (Source: U.S. Nuclear Regulatory Commission)

Though there has been an aforementioned stalling of new nuclear construction, there are currently two new reactors set for operation sometime in 2023 and 2024. If system difficulties and delays cease to persist, Georgia’s Vogtle Units 3 and 4 will be the newest operating reactors since Watts Bar Unit 2 in 2016. These units will add about 2,500 MW to the state’s energy mix. The completion of these reactors is seen as a critical step for future advancements in U.S. civilian nuclear as well as the nation’s position as a global nuclear leader, according to the U.S. DOE. The power plant additions in Georgia were made possible by almost $12 billion in loans that were issued by the U.S. DOE’s Loan Program Office, and are just some of the different financial assistance streams that the federal government gives to nuclear power.

Besides the DOE’s support, multiple financial incentives for nuclear power were passed in 2021 via the Infrastructure Investment and Jobs Act (IIJA) and via the Inflation Reduction Act (IRA) last year. The IIJA created the Civil Nuclear Credit Program, which allows owners/operators of commercial reactors that demonstrate a projected shutdown for economic reasons to apply for certification and bid on credits that support continued operations. The application must also demonstrate that suspending reactor operations will lead to increased air pollution and carbon emission levels. Applicants are only given a credit if the U.S. Secretary of Energy, in consultation with the NRC, determines with enough assurance that the continuation of operations does not present any critical danger or hazard. The program’s credits are allocated through four-year periods, with the program expiring on September 30, 2031 – unless funds run out earlier. The purpose of the Civil Nuclear Credit Program is to halt potential, early closures of commercial nuclear power reactors due to the pattern of shutdowns as a result of economic shifts; and to achieve the country’s goal of achieving a carbon-free electricity sector by 2035 and net-zero emissions by 2050.

The program announced the first selection in November 2022, that being California's Diablo Canyon Units 1 and 2, which were set for decommissioning in 2024/2025 and produce 15% of the state’s clean energy. The west-coast power plant was awarded a credit value of up to $1.1 billion, as the plant tries to extend its lifespan. Recently, the NRC announced that Pacific Gas & Electric Co. (PG&E), which operates the Diablo Canyon units, has to resubmit a license renewal application after the Commission rejected the company’s request to resume its renewal application from 2009. In September 2022, the California legislature voted to extend operations of the state’s only and remaining plant, and gave PG&E a $1.4 billion loan for its plant. Last month, the state’s Public Utilities Commission opened a rulemaking on whether to extend the plant’s units through 2029/2030. If given approval from the NRC and the state Commission, Diablo Canyon’s $1.1 billion credit will help it resume operations.

As for the IRA, it also provided current nuclear power plants with a plethora of financial incentives to take advantage of. The legislation establishes a Zero-Emission Nuclear Power Production Tax Credit (Section 45U) of $15/MWh for electricity produced starting in 2024. However, in order to receive the full credit, plants must meet labor and prevailing wage requirements. The production credit is meant to operate under current market conditions, and will gradually decrease as power prices reach above $25/MWh. The IRA even revives the Qualifying Advanced Energy Project Credit (Section 48C), for eligible facilities such as equipment designed to refine, electrolyze, or blend any chemical, fuel, or a product that is low carbon/emission, among others. It gives the U.S. Department of the Treasury the authority to utilize a max $10 billion worth of credits – and $6 billion max for projects outside of energy communities – for these facilities. The tax credit covers 30% of the cost, but is reduced if wage and apprenticeship standards are not achieved. There is also the Advanced Manufacturing Production Tax Credit (Section 45X), for eligible components produced and sold after 2022; including finished equipment and component parts of electricity inverter equipment, among others. The credit rate varies based on the type of component.

Besides the incentives and support from the IRA have been mentioned above, there is also the Advanced Nuclear Tax Credit (Section 45J) that was added under the Energy Policy Act of 2005. This incentive offers a max credit of 1.8 cents/kWh, and was amended by the Bipartisan Budget Act of 2018, granting facilities placed into service after December 31, 2020 eligibility under the credit. Additionally, individual states have also instituted their own financial incentives for nuclear power developers, due to the fact that they can levy property and sales taxes. States like Kansas, Nebraska, New York, and Wyoming, have given property tax exemptions to either nuclear generation facilities or fuel.

The numerous financial incentives offered by the federal government and some states are keeping stakeholders from being discouraged when it comes to constructing and financing nuclear power plants. The DOE recognizes that standard reactor designs are multi-billion dollar projects, with high capital costs, and lengthy licensing and regulation processes. The agency also posits that long timelines and construction delays have dampened public interest in the power type; and that the nuclear industry is struggling to compete with other energy sources due to a combination of market conditions. Knowing this, the DOE is helping in supporting a new generation of advanced nuclear technologies.

Nuclear’s Future

The next generation of reactors, often categorized as either Gen IV or advanced reactors, are seeing more and more commercial and governmental support – such as the DOE – as an answer to current economic and infrastructural issues. When it comes to the reactors that are operational today and have been extended into the future, most are Gen II (which began operation in the late 60s and are typically the light water reactors we see today) and some Gen III (which improve upon Gen II through improvements in fuel tech, thermal efficiency, safety systems, etc.; although none are currently operational in the U.S.), having learned and upgraded from the Gen I early prototype reactors. Then there is Gen IV, which offers varying types of reactor designs and sizes equipped with different coolant mechanisms and safety measures, among other specifications. Currently, there are several examples of these types that are being drafted and prepped for possible licensing, construction, and demonstrations, as more and more capital is gathered by interested developers. Below is a list of some of the more prominently known advanced reactors technologies:

|

Reactor Type

|

Description

|

|

Small Modular Reactors (SMRs)

|

Differently sized reactors that are less than 300 MW; can be made using non-water or water coolant technology; factory-built and use passive safety features

|

|

Molten Salt Reactors (MSRs)

|

Non-water-cooled reactors that use molten salt as a coolant; sizes currently vary from less than 300 MW to 600 MW

|

|

Sodium-Cooled Fast Reactors (SFRs)

|

Non-water-cooled reactors that use liquid sodium; sizes currently vary from 50-1,500 MW

|

|

Lead-Cooled Fast Reactors (LFRs)

|

Non-water-cooled reactors that use molten lead or lead-bismuth eutectic; sizes currently vary from 25 MW to 450 MW

|

|

Gas-Cooled Fast Reactors (GFRs)

|

Non-water-cooled reactors that use helium; sizes currently vary from 0.5 MW to 2,400 MW of thermal power

|

|

High-Temperature Gas Reactors (HTGRs)

|

Non-water-cooled reactors that use helium as a coolant, while operating at high temperatures; sizes are currently under 300 MW

|

|

Supercritical Water-Cooled Reactors (SCWRs)

|

Water-cooled reactors that use supercritical water, which is a fourth state of material appearing as a vapor; sizes currently vary between 300 and 1,700 MW

|

|

Micro-Reactors

|

Differently sized reactors that are less than 50 MW; mobile, deployable, and can be the size of a flatbed truck

|

|

Fusion Reactors

|

Use nuclear fusion as a power source, during which two atoms collide, creating a net energy gain; can be made using non-water or water coolant technology; theoretical size is 500 MW

|

Some of these advanced reactors have already gained traction in the U.S. In January, the NRC approved the first SMR advanced reactor design, NuScale’s advanced light-water SMR. The final ruling was made effective at the end of this year, and is a gradual start to commercializing and constructing advanced reactors in the U.S. NuScale is working with the Utah Associated Municipal Power Systems on an SMR project consisting of six-modules at Idaho National Laboratory. The six-SMR project would generate at a capacity of about 462 MW, with one module having a 77 MW capacity. Additionally, Nebraska, with federal funding from the American Rescue Plan Act, recently began a siting study for potential SMRs in the state. Also, the first commercial contract for an SMR in North America was signed in Canada. Companies, including Ontario Power Generation, GE Hitachi, SNC-Lavalin, and Aecon are partnering together on the project, and is planned for the Darlington site in Clarington, Ontario.

Image (above) of an artist’s rendering of NuScale’s SMR plant. (Source: NuScale/U.S. Department of Energy)

As for other advanced reactors, the Bill Gates-founded company TerraPower is looking to replace the soon-to-be decommissioned coal-fired power plant in Kemmerer, Wyoming. The planned but not-yet licensed sodium-cooled fast reactor utilizes High-Assay Low-Enriched Uranium (HALEU), which is a type of uranium fuel that is enriched between 5-20% and required for most U.S. advanced reactors. As of now, HALEU can only be commercially-sourced from Russia, leaving the project without a fuel source and has caused project delays. Fortunately for this type of fuel, the IRA has allocated $700 million in funding to the DOE for the development of a domestic HALEU supply chain.

As for the plant design, it utilizes a molten salt energy storage system, which is heated and stored in insulated container units and then pumped into a steam generator, spinning a turbine and generating electricity. West Virginia, which repealed a decades-old law last year that prohibited nuclear power production in the state, is also showing interest in collaborating with TerraPower for possible future development of a sodium-cooled fast reactor. Meanwhile, Maryland-based X-energy is developing an HTGR that is expected to reach the operational stage by 2028. Both TerraPower and X-energy receive funding from the DOE’s Advanced Reactor Demonstration Program, which was recently appropriated an extra $2.5 billion through the IIJA. Then there is the recent scientific success of reproducing a fusion reaction similar to the sun. The reaction, discovered at the $3.5 billion National Ignition Facility Lawrence Livermore National Laboratory in California, created 3 MJ worth of energy out of 2.05 MJ of energy used. The project utilized 192 giant lasers after having begun operations in 2009.

Advanced reactors have also been given financial incentives through the IRA, to assist in the economics of future reactors. The legislation’s Clean Electricity Investment Tax Credit (Section 48E) offers facilities placed in service starting 2025 a credit that is equal to 6% of a qualified investment in a qualified facility, which goes up to 30% once prevailing wage and apprenticeship standards are met; with additional bonus credits for siting in an energy community, meeting domestic content standards, and being placed in low-income or tribal communities. The IRA also amends the Clean Electricity Production Tax Credit (Section 45Y) and opens up a pathway for advanced reactors to participate, similarly to Section 48E. The amendment changes the eligible operation date for 2025 and after. The production tax credit offers facilities a credit of up to $15/MWh, and is also eligible for bonus credits. The 2022 legislation also contains the technology-neutral Clean Hydrogen Production Tax Credit (Section 45V); which can also be utilized by nuclear facilities that produce hydrogen – otherwise known as pink hydrogen. The credit gives qualifying production facilities that begin construction starting 2023 and before 2033 an inflation adjusted credit rate for 10 years, ranging from $0.12/kg (or 20% of the credit) to $0.60/kg of hydrogen (the full credit). The credit is expanded five-fold if prevailing wage and apprenticeship standards are met.

With the number of incentives available to advanced reactors and the commercial potential of a number of designs gradually increasing, Gen IV reactors are being looked at more closely as an alternative to past designs. Even the DOE found that almost 80% of retired and operating coal plant sites are good candidates for the coal-to-nuclear transition, especially for hosting advanced reactors below a GW like SMRs. The DOE’s report on investigating the benefits and challenges of coal plant conversion into nuclear plants found that emissions in regions that undergo this transition see an 86% emission reduction – equal to more than 500,000 combustion passenger vehicles being taken off the road. The report also finds that applicable regions could see more than 650 long-term jobs open up, alongside a possible yearly economic influx of $275 million, and a 92% tax revenue increase for municipalities and counties that choose to transition versus continuing coal power operations.

(Source: U.S. Energy Information Administration)

Even so, the EIA finds that nuclear electricity generation might fall to 12% in 2050, compared to 19-20% of the nation’s electricity in the last couple of years, as renewables are projected to double in share. What puts this projection in limbo is the NRC’s current rulemaking regarding a regulatory framework for advanced reactors. The rulemaking would establish an optional technology-inclusive regulatory framework that can be used by new commercial advanced nuclear reactor applicants, utilizing risk-informed and performance-based methods to be considered flexible and practicable for a host of advanced technologies. The proposed rule publication date is set for August 28, 2023, after comments were due around the same time last year. The final rule is set for publication on June 27, 2025. The rulemaking is important for advanced nuclear developers that want to expand and construct in the U.S. under a given regulatory framework, and will have a significant impact on Gen IV’s domestic development. Overall, through the recent wave of incentives, pursuits of advanced reactors, and support for future nuclear technologies, nuclear’s future is being given a signal of support. However, the impact of this support will still largely depend on some of the same factors that have impacted civilian nuclear for the last 60+ years, specifically the economics and regulation of a new generation.

Contact us to learn about our DSIRE Insight subscriptions, as well as custom research and consulting offerings on a variety of clean energy technologies for persons/organizations interested.